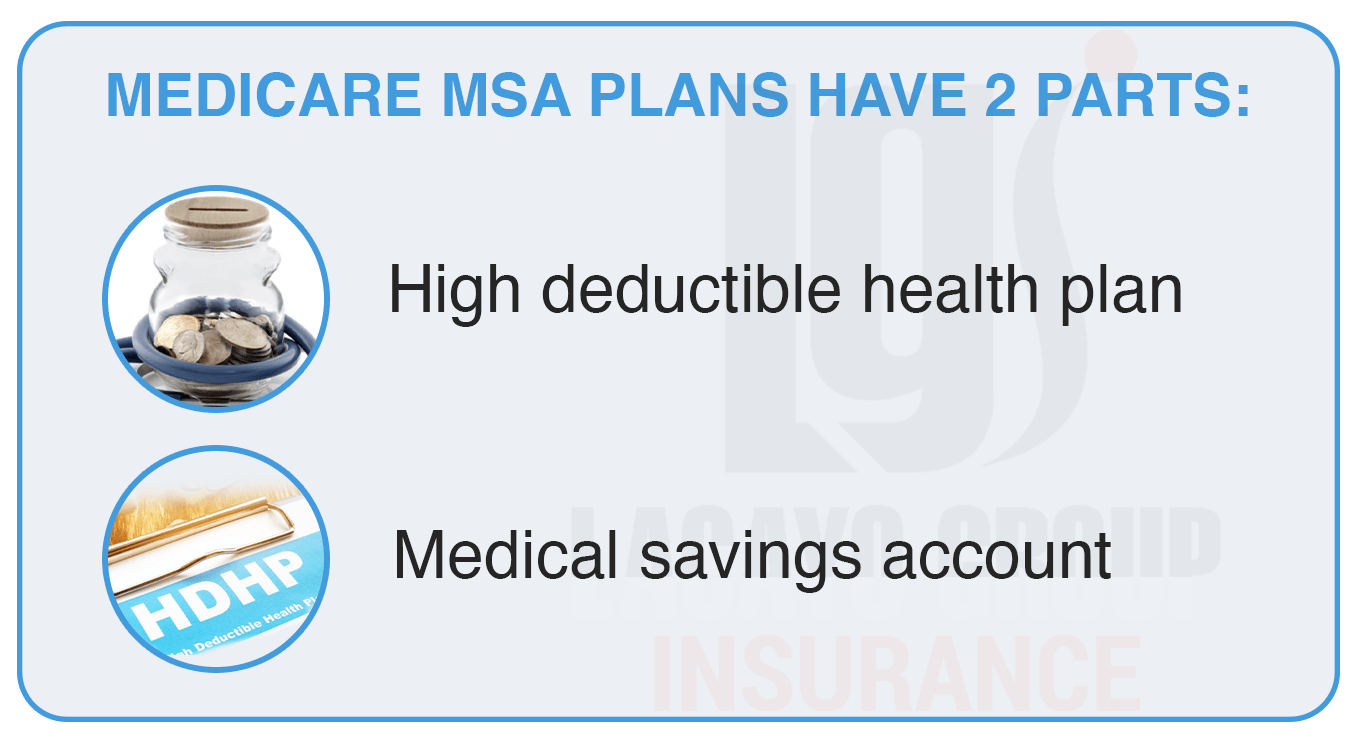

Medicare Medical Savings Account Loans

Medicare covers many of your medical expenses after you turn 65. However, there are some things it does not cover, which is why beneficiaries in Florida and Texas often choose a Medicare Advantage plan or a Medicare Supplement plan. This page will focus on a particular type of Medicare Advantage (Part C) plan: Medical Savings Account loans or MSAs for short.

Who’s Eligible for a Medicare MSA?

If you have Original Medicare (Parts A and B), you may qualify for a high-deductible MSA plan, which uses a flexible savings account funded by the government each year.

If any of these apply to you, you’re INELIGIBLE:

- You’re in hospice care

- You qualify for Texas or Florida Medicaid

- You have End-Stage Renal Disease

- You live outside the U.S. for half the year or more

- You already have health insurance that would cover some or all of your annual deductible